Boiler and Machinery Coverage: A Practical 2026 Comparison

A detailed, balanced comparison of basic vs. comprehensive boiler and machinery coverage for homeowners and facilities. Learn what’s covered, key terms, policy design, cost factors, and how to file claims to protect equipment and uptime.

A comprehensive boiler and machinery coverage plan generally offers the best protection by combining equipment breakdown protection with downtime, business interruption elements, and optional endorsements. For most homeowners and facilities, a broad yet carefully scoped policy balances risk and cost more effectively than a bare-bones option. Endorsements for critical equipment and clear exclusions review are essential for maximizing value.

The stakes of boiler and machinery coverage

According to Boiler Hub, boiler and machinery coverage is a cornerstone of risk management for facilities that rely on steam, hot water, or other heat-producing systems. When a boiler fails or a related machine breaks, downtime can quickly cascade into lost production, delayed maintenance, and safety concerns. The right coverage helps manage repair costs, protect uptime, and keep compliance on track. In practical terms, this type of coverage shifts unpredictable repair bills from your balance sheet to an insured risk transfer, which can preserve cash flow and support budgeting over the policy period. For homeowners with advanced systems or small businesses with multi-equipment plants, the protection afforded by boiler and machinery coverage reduces the financial shock of breakdowns and aligns with broader risk strategies.

This section also helps set the framework for understanding the two primary paths you’ll consider: basic coverage and comprehensive boiler and machinery coverage. Both paths aim to reduce exposure to equipment failure and downtime, but they differ in scope, endorsements, and the degree of protection you receive. The choice often hinges on the size of the operation, the criticality of the equipment, and the potential downstream impact of a disruption. The Boiler Hub team emphasizes that a well-chosen policy should integrate seamlessly with existing maintenance practices and incident response plans.

Brand context note: The Boiler Hub team recommends starting with a clear inventory of all equipment and a risk assessment to map coverage needs to your specific operation. This practice supports a cleaner underwriting process and better long-term value.

mainTopicQuery2Text

Comparison

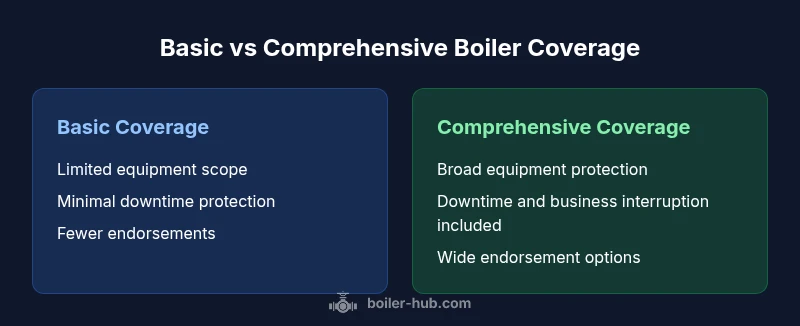

| Feature | Basic Boiler Coverage | Comprehensive Boiler & Machinery Coverage |

|---|---|---|

| Equipment Coverage | Limited to boiler itself and a narrow set of connected devices | Broad coverage including ancillary equipment, pumps, valves, controls, and related systems |

| Downtime Protection | Limited downtime protection, if any | Broader business interruption provisions tied to equipment breakdown |

| Endorsements Access | Fewer optional endorsements | Wide range of endorsements for critical equipment and scenarios |

| Exclusions & Limits | More exclusions and lower aggregate limits | Fewer exclusions and higher aggregate protection |

| Maintenance & Compliance | Standard maintenance may be required | Flexible maintenance requirements with risk-based tailoring |

| Cost/Value Balance | Lower upfront cost, simpler policy | Higher premium but greater overall protection and resilience |

| Best For | Small facilities or homeowners with minimal risk | Medium to large operations needing comprehensive protection |

Advantages

- Reduces out-of-pocket repair costs for boiler and connected equipment

- Helps limit downtime losses with business interruption coverage

- Endorsements tailor protection to critical equipment and specific risk factors

- Improves lender and insurer confidence through stronger risk management

- Supports compliance with safety and regulatory requirements

The Bad

- Premiums can be higher for comprehensive plans

- Coverage gaps may exist if the policy isn’t reviewed carefully

- Claims can require extensive documentation and timely reporting

- Endorsements add complexity and require careful management

Comprehensive boiler and machinery coverage generally wins for mid-to-large operations; basic coverage may suit small-scale risk with tight budgets

For most homeowners and facilities, a broad boiler and machinery policy offers stronger protection against both repair costs and downtime. Endorsements should be matched to critical equipment, and a careful review of exclusions helps close gaps. The Boiler Hub team’s assessment is that the comprehensive approach provides the best value when downtime risk is material and equipment spans multiple subsystems.

Questions & Answers

What is boiler and machinery coverage, and who needs it?

Boiler and machinery coverage protects equipment used in heating, power, and related processes. It covers repair or replacement costs due to breakdowns and, in many cases, losses from downtime. It is especially relevant for facilities with boilers, pumps, and control systems, as well as homeowners with complex or mission-critical heating equipment. If your operation depends on continuous mechanical performance, this coverage can prevent large, unexpected expenses.

Boiler and machinery coverage protects essential heating and mechanical equipment from breakdown costs, reducing downtime risk for facilities and homes with complex systems.

What does this coverage usually include and exclude?

Typical inclusion covers boiler equipment and connected machinery, controls, and sometimes related electrical components. Common exclusions may involve wear-and-tear, improper maintenance, and pre-existing conditions, depending on policy language. Always review the exclusions list and confirm whether business interruption is tied to uptime rather than solely to the equipment’s physical condition.

Check what’s covered, especially for controls and auxiliary equipment, and read exclusions carefully to avoid gaps.

How do endorsements affect boiler coverage?

Endorsements customize protection to your risk profile, adding coverage for stair-step scenarios, seasonal operations, or high-value equipment. They can broaden protection for downtime, add coverage for rented equipment, or cover specific failures not included in standard forms. Endorsements often affect premium and claim procedures, so choose them to align with real risk exposure.

Endorsements tune protection to real risk—choose ones that cover your critical equipment and likely failure scenarios.

How is the premium determined for boiler and machinery coverage?

Premiums are driven by equipment value, reliability, installation complexity, location, and the operational risk profile. A facility with multiple high-risk machines or older equipment will generally face higher rates. Bundling with other policies or implementing preventive maintenance programs can influence pricing.

Premiums depend on equipment value, risk, and maintenance practices; proactive risk management can help control costs.

What are common pitfalls to avoid when choosing coverage?

Common issues include underinsuring due to a narrow equipment list, not aligning endorsements with actual risk, and neglecting to review exclusions and limits. Also, ensure your incident response and documentation processes are aligned with the insurer’s requirements to avoid claim delays.

Avoid gaps by listing all critical equipment, confirming endorsements, and planning for timely claim documentation.

Key Points

- Start with a complete equipment inventory to align coverage

- Prioritize endorsements for critical machinery and controls

- Balance premium cost with potential downtime exposure

- Review exclusions and limits to close protection gaps

- Involve your insurer early in policy design to tailor coverage